All Categories

Featured

Table of Contents

Below is a theoretical contrast of historical performance of 401(K)/ S&P 500 and IUL. Allow's think Mr. SP and Mr. IUL both had $100,000 to saved at the end of 1997. Mr. SP spent his 401(K) cash in S&P 500 index funds, while Mr. IUL's money was the money worth in his IUL plan.

IUL's policy is 0 and the cap is 12%. Given that his money was saved in a life insurance plan, he does not require to pay tax!

Panet Co Iul

Life insurance pays a fatality advantage to your recipients if you should die while the plan is in result. If your family members would deal with financial challenge in the occasion of your death, life insurance provides peace of mind.

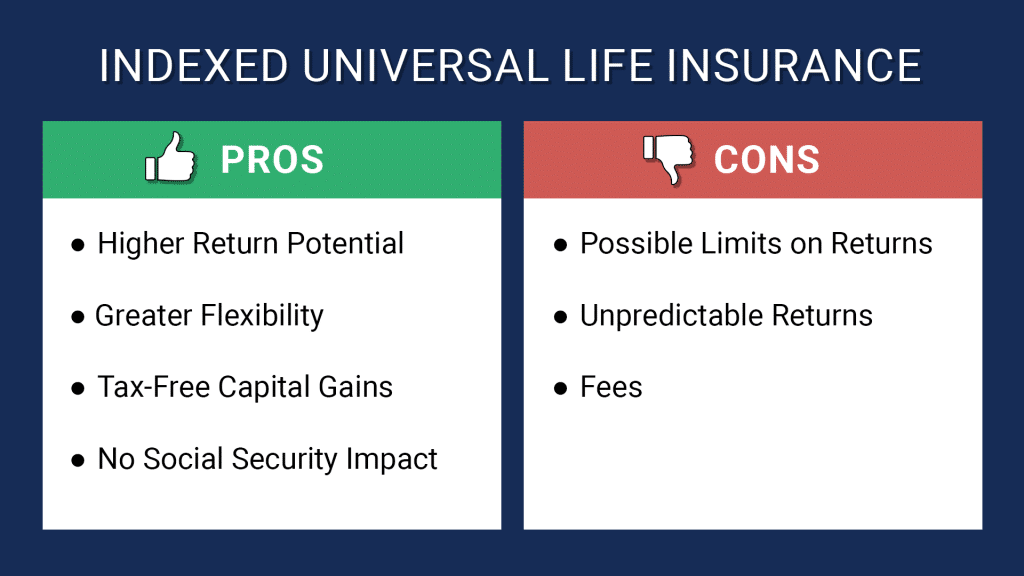

It's not one of the most lucrative life insurance policy investment strategies, however it is one of one of the most safe. A form of long-term life insurance coverage, universal life insurance coverage permits you to select just how much of your costs approaches your death benefit and how much enters into the plan to accumulate cash value.

In addition, IULs permit policyholders to take out financings against their plan's cash value without being taxed as earnings, though unpaid balances might undergo tax obligations and charges. The key benefit of an IUL plan is its potential for tax-deferred growth. This means that any type of revenues within the plan are not strained until they are withdrawn.

Conversely, an IUL plan may not be the most suitable cost savings prepare for some people, and a traditional 401(k) might confirm to be extra useful. Indexed Universal Life Insurance Coverage (IUL) policies offer tax-deferred development potential, defense from market slumps, and fatality benefits for beneficiaries. They enable policyholders to make rate of interest based upon the efficiency of a securities market index while securing against losses.

Indexed Universal Life Or 401k For Long-term Savings

Companies might likewise provide matching contributions, further enhancing your retirement cost savings capacity. With a standard 401(k), you can minimize your taxed revenue for the year by adding pre-tax bucks from your income, while likewise benefiting from tax-deferred development and company matching contributions.

Several employers likewise provide matching contributions, efficiently providing you complimentary cash towards your retirement. Roth 401(k)s function similarly to their typical equivalents but with one trick distinction: taxes on payments are paid upfront rather of upon withdrawal throughout retirement years (iul vs 401k calculator). This indicates that if you expect to be in a greater tax obligation bracket throughout retired life, adding to a Roth account might save money on tax obligations over time compared to investing solely via standard accounts (resource)

With reduced administration fees generally compared to IULs, these sorts of accounts allow investors to save cash over the lengthy term while still gaining from tax-deferred development capacity. Furthermore, numerous popular affordable index funds are available within these account types. Taking circulations before getting to age 59 from either an IUL policy's cash money worth by means of loans or withdrawals from a conventional 401(k) plan can lead to negative tax obligation implications if not taken care of thoroughly: While borrowing against your plan's money worth is normally considered tax-free as much as the amount paid in costs, any type of overdue funding equilibrium at the time of fatality or policy surrender may undergo income tax obligations and charges.

Can You Maximize Your Retirement By Using Both Iul And 401(k)?

A 401(k) supplies pre-tax investments, employer matching payments, and potentially more investment selections. The drawbacks of an IUL consist of greater management costs contrasted to standard retired life accounts, limitations in financial investment choices due to policy restrictions, and possible caps on returns throughout strong market efficiencies.

While IUL insurance policy might show important to some, it's essential to recognize just how it works before acquiring a plan. There are a number of pros and cons in contrast to various other kinds of life insurance policy. Indexed global life (IUL) insurance policies provide higher upside potential, versatility, and tax-free gains. This sort of life insurance policy provides permanent coverage as long as premiums are paid.

companies by market capitalization. As the index moves up or down, so does the price of return on the cash money value component of your plan. The insurer that provides the plan may provide a minimum surefire price of return. There might likewise be a ceiling or rate cap on returns.

Economists usually encourage living insurance policy protection that amounts 10 to 15 times your annual revenue. There are several disadvantages related to IUL insurance plan that doubters fast to mention. A person who develops the policy over a time when the market is performing improperly can finish up with high costs repayments that don't contribute at all to the cash worth.

In addition to that, bear in mind the adhering to various other considerations: Insurance provider can set engagement prices for just how much of the index return you obtain annually. Allow's say the plan has a 70% engagement rate. If the index grows by 10%, your cash money value return would certainly be just 7% (10% x 70%)

Furthermore, returns on equity indexes are usually covered at a maximum quantity. A plan might say your optimum return is 10% each year, despite exactly how well the index does. These restrictions can restrict the actual rate of return that's attributed towards your account each year, regardless of how well the plan's hidden index does.

What Are The Key Differences Between Iul And 401(k)?

Yet it's vital to consider your individual threat resistance and investment objectives to ensure that either one aligns with your general approach. Whole life insurance policy policies typically consist of a guaranteed rates of interest with foreseeable premium amounts throughout the life of the policy. IUL plans, on the various other hand, offer returns based upon an index and have variable costs with time.

There are many other sorts of life insurance plans, explained listed below. uses a set advantage if the insurance policy holder passes away within a set duration of time, generally between 10 and 30 years. This is among the most affordable kinds of life insurance policy, as well as the simplest, though there's no cash money worth build-up.

Understanding Indexed Universal Life Insurance (Iul) Vs. Roth Ira

The policy gains value according to a repaired schedule, and there are fewer costs than an IUL policy. They do not come with the adaptability of readjusting costs. comes with even more versatility than IUL insurance coverage, indicating that it is also much more complicated. A variable policy's cash worth may depend on the performance of particular supplies or various other protections, and your premium can likewise change.

%20Over%20A%20401(k)){kind=link}

Latest Posts

Index Life Insurance Companies

Is Iul Good Investment

Best Variable Universal Life Insurance Policy